Unexpected expenses are one of the most common reasons people experience financial stress. Whether it is a medical emergency, car repair, home maintenance issue, or temporary loss of income, unplanned costs can disrupt even the most carefully designed budget. Learning the Emergency Expense Planning can help you protect your finances and avoid unnecessary debt.

Financial emergencies are often unavoidable, but their impact can be reduced through preparation and planning. Individuals who prepare in advance typically recover more quickly and experience less financial stress when unexpected costs arise.

In 2026, rising living expenses and economic uncertainty make financial preparedness more important than ever. Fortunately, several practical strategies can help create financial resilience and improve long-term stability.

The Emergency Expense Planning focus on saving, budgeting, risk management, and financial planning.

Why Unexpected Expenses Matter

Unexpected costs can affect anyone regardless of income level.

Common examples include:

- Medical emergencies

- Vehicle repairs

- Home maintenance

- Job loss

- Family emergencies

Without preparation, these situations can lead to debt and financial setbacks.

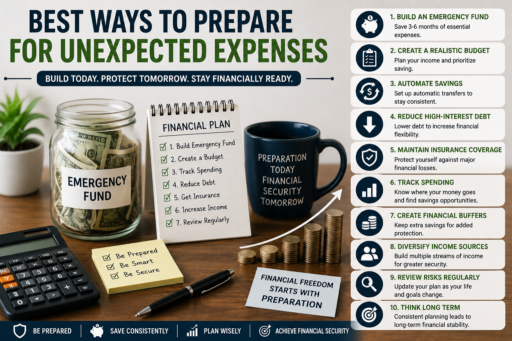

Way #1: Build an Emergency Fund

The most important strategy among the Emergency Expense Planning is building an emergency fund.

An emergency fund can help cover:

- Medical costs

- Repair expenses

- Temporary income loss

- Unexpected financial emergencies

Even a modest emergency fund can significantly improve financial security.

Way #2: Create a Realistic Budget

A budget helps identify opportunities to save money and prepare for future challenges.

Your budget should include:

- Essential expenses

- Savings contributions

- Debt payments

- Emergency savings allocations

Strong budgeting habits often improve financial preparedness.

Way #3: Automate Savings Contributions

Automatic savings transfers help ensure emergency funds continue growing consistently.

Automation reduces the temptation to spend money intended for savings.

People who follow the Emergency Expense Planning often rely on automated systems to maintain consistency.

Way #4: Reduce High-Interest Debt

Debt can limit financial flexibility during emergencies.

Prioritize reducing:

- Credit card balances

- High-interest loans

- Costly financing arrangements

Lower debt levels provide greater financial resilience.

Way #5: Maintain Insurance Coverage

Insurance helps protect against large financial losses.

Important coverage may include:

- Health insurance

- Auto insurance

- Home insurance

- Life insurance

Insurance is an important component of financial risk management.

Way #6: Track Spending Carefully

Understanding spending patterns helps identify opportunities to strengthen financial preparedness.

Monitor:

- Monthly expenses

- Subscriptions

- Discretionary spending

- Saving opportunities

Awareness often leads to stronger financial decisions.

Way #7: Create Financial Buffers

Financial buffers provide additional protection beyond emergency savings.

Examples include:

- Extra savings accounts

- Flexible budget categories

- Cash reserves

- Short-term savings goals

Additional financial reserves improve stability.

Way #8: Diversify Income Sources

Relying on a single source of income can increase financial vulnerability.

Additional income sources may include:

- Freelance work

- Part-time opportunities

- Side businesses

- Investment income

Multiple income streams often improve financial security.

Way #9: Review Financial Risks Regularly

Financial risks change over time.

Review:

- Insurance needs

- Savings balances

- Debt obligations

- Income stability

Regular reviews help ensure continued preparedness.

Way #10: Think Long Term

Financial preparedness is not a one-time activity.

Consistent saving, budgeting, and planning can create long-term resilience against unexpected expenses and financial emergencies.

Common Mistakes People Make During Financial Emergencies

Unexpected expenses often lead to poor financial decisions when people are unprepared.

Common mistakes include:

- Using high-interest credit cards

- Borrowing unnecessarily

- Ignoring emergency savings

- Failing to review insurance coverage

- Panicking and making rushed decisions

The Emergency Expense Planning help reduce the likelihood of these costly mistakes.

Focus on Prevention Whenever Possible

While not every emergency can be avoided, some unexpected expenses can be reduced through preventative actions.

Examples include:

- Regular vehicle maintenance

- Home inspections

- Routine medical checkups

- Equipment maintenance

People who use the Emergency Expense Planning often focus on prevention as well as preparation.

Strengthen Your Emergency Fund Over Time

Emergency funds should continue growing as financial responsibilities increase.

Factors that may require larger emergency savings include:

- Family responsibilities

- Home ownership

- Business ownership

- Higher monthly expenses

Growing emergency savings can improve long-term financial resilience.

Create a Financial Emergency Plan

A financial emergency plan helps reduce stress during difficult situations.

Your plan may include:

- Emergency contact information

- Important account details

- Insurance information

- Emergency savings locations

- Priority expense lists

The Emergency Expense Planning often include creating systems before emergencies occur.

Keep Essential Financial Documents Organized

Important financial information should be easy to access when needed.

Examples include:

- Insurance policies

- Bank account information

- Investment account details

- Emergency contacts

- Budget records

Organization can save valuable time during stressful situations.

Build Financial Flexibility

Financial flexibility allows individuals to adapt more easily to changing circumstances.

Ways to increase flexibility include:

- Reducing fixed expenses

- Maintaining cash reserves

- Avoiding excessive debt

- Building multiple income streams

Greater flexibility often reduces the impact of unexpected costs.

Review Emergency Preparedness Annually

Financial circumstances change over time.

Review annually:

- Emergency fund balances

- Insurance coverage

- Budget structure

- Financial risks

- Income stability

People who follow the Emergency Expense Planning often update their plans regularly to remain prepared.

Maintain a Long-Term Perspective

Unexpected expenses can feel overwhelming, but they are often temporary challenges.

A strong financial foundation helps individuals recover more quickly and continue making progress toward long-term goals.

Preparation creates confidence and reduces uncertainty.

Use Trusted Financial Resources

Individuals interested in strengthening financial preparedness can benefit from trusted educational resources. The Consumer Financial Protection Bureau provides practical guidance on budgeting, saving, debt management, and emergency financial planning.

Reliable financial education can improve decision-making during both normal and challenging financial situations.

Additional Resources for Financial Stability

To strengthen your financial preparedness, consider reading Improve Financial Discipline, Save More Money Every Month, and Money Management Tips for Singles.

These resources provide practical strategies that complement the emergency preparation techniques discussed in this guide.

The Benefits of Being Financially Prepared

Following the Prepare for Unexpected Expenses can provide:

- Greater financial security

- Reduced financial stress

- Improved emergency preparedness

- Better financial confidence

- Long-term financial stability

Preparation helps individuals respond to unexpected challenges with confidence and resilience.

Final Thoughts

The Emergency Expense Planning can help individuals build stronger financial foundations and reduce the impact of future financial emergencies.

By building emergency savings, maintaining insurance coverage, reducing debt, tracking expenses, and creating financial systems, you can improve your financial preparedness and protect your long-term goals.

Remember that financial resilience is built gradually. Small steps taken consistently today can provide significant protection tomorrow.