Imagine applying for a mortgage, auto loan, or new credit card only to discover an unexpected problem on your credit report. To avoid surprises like these, it’s important to Monitor Your Credit Effectively. Maybe an old account is reporting incorrect information. Perhaps a fraudulent account was opened without your knowledge. Or maybe your credit utilization quietly increased over several months without you paying attention.

Situations like these happen more often than many people realize. The frustrating part is that most credit problems do not appear overnight. In many cases, warning signs exist for months before consumers notice them.

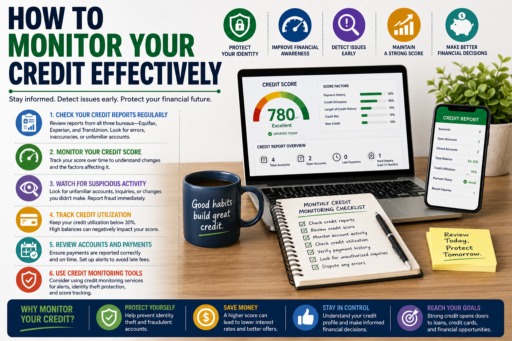

This is why learning how to Monitor Your Credit Effectively is such an important financial skill. Credit monitoring is not only about protecting your score. It is about understanding your financial profile, identifying potential problems early, tracking progress, and making informed financial decisions.

Many people spend years trying to improve their credit but only a few minutes each year reviewing it. Unfortunately, that approach can allow small issues to become expensive mistakes.

In this guide, you’ll learn practical strategies for monitoring your credit, recognizing warning signs, protecting your financial identity, and maintaining long-term credit health.

Why Credit Monitoring Matters More Than Most People Think

Many consumers assume that credit monitoring is only necessary when applying for a loan.

In reality, your credit profile is constantly changing.

Balances change. Accounts age. New information is reported. Credit utilization fluctuates. Financial habits leave a trail that gradually shapes your credit profile.

Without regular monitoring, important changes can go unnoticed.

Think of credit monitoring the same way you think about routine health checkups. Most people do not wait until they are seriously ill before seeing a doctor. Likewise, waiting until you need financing before reviewing your credit can create unnecessary surprises.

Effective monitoring helps you:

- Track credit score progress.

- Detect reporting errors.

- Identify potential fraud.

- Monitor utilization changes.

- Protect long-term financial health.

- Maintain confidence when applying for credit.

What Information Should You Monitor?

One of the biggest misconceptions about credit monitoring is that it only involves checking a credit score.

Your score is important, but it is only one piece of a much larger picture.

Consumers who successfully Monitor Your Credit Effectively often review several key areas:

- Payment history.

- Credit utilization.

- Open accounts.

- Closed accounts.

- Credit inquiries.

- Personal information.

- Reported balances.

Looking beyond the score often provides valuable insights that numbers alone cannot reveal.

The Difference Between Monitoring and Obsessing

Interestingly, some consumers make the opposite mistake.

Instead of ignoring credit, they check it constantly.

Imagine stepping on a scale every hour while trying to lose weight. The constant monitoring would likely create stress without providing useful information.

Credit works similarly.

Checking your profile regularly is helpful. Checking it obsessively often adds anxiety without improving results.

For most people, monthly reviews are more than enough to stay informed while maintaining perspective.

How to Spot Credit Report Errors Early

One of the biggest benefits of credit monitoring is the ability to catch mistakes before they become serious problems.

Many consumers assume that everything appearing on a credit report is accurate. While most information is reported correctly, errors can occur.

Imagine applying for a loan only to discover that an old account is incorrectly listed as unpaid. Or perhaps a balance appears much higher than it actually is.

These situations can be frustrating, especially if they remain unnoticed for months.

When reviewing your credit information, pay attention to:

- Account balances.

- Payment history.

- Account status.

- Personal information.

- Recently opened accounts.

Even small inaccuracies deserve attention because they may affect your overall credit profile.

Detecting Fraud Before It Becomes Expensive

Fraud is another reason why consumers should monitor their credit regularly.

Identity theft often begins quietly.

An unfamiliar inquiry may appear.

A new account might be opened without your knowledge.

A balance could suddenly increase for reasons you cannot explain.

The sooner suspicious activity is identified, the easier it usually becomes to address.

Think of credit monitoring as an early-warning system. It cannot prevent every problem, but it can help you respond faster when something unusual occurs.

People who Monitor Your Credit Effectively often discover issues long before they become major financial headaches.

Why Credit Utilization Should Be Monitored Monthly

Many consumers pay attention to balances but ignore utilization.

This can be a costly mistake.

Imagine you normally keep utilization around 15%.

Then an unexpected expense causes balances to rise.

A few months later, utilization reaches 60% without you realizing it.

Your score may begin feeling the impact even though you never missed a payment.

This is why utilization deserves regular attention.

Monthly monitoring allows you to identify trends before they become larger problems.

Related Article: How Credit Utilization Affects Your Score

Track Progress Instead of Chasing Perfection

One mistake many people make is expecting perfect credit immediately.

Credit improvement is usually gradual.

Instead of focusing only on the final destination, monitor progress along the way.

Positive signs may include:

- Lower utilization.

- Fewer outstanding balances.

- Longer account history.

- Consistent payment records.

- Improved financial organization.

These trends often matter more than short-term fluctuations.

People who focus on steady improvement usually maintain stronger financial habits over time.

Creating a Monthly Credit Monitoring Routine

The best monitoring systems are simple enough to maintain consistently.

You do not need complicated spreadsheets or expensive tools.

A monthly routine might include:

- Review all credit card balances.

- Check utilization percentages.

- Verify upcoming due dates.

- Review recent account activity.

- Look for unfamiliar inquiries.

- Track long-term credit goals.

This process typically takes less than thirty minutes each month but can significantly improve financial awareness.

A Real-Life Example of Effective Credit Monitoring

Consider two consumers with similar financial situations.

The first rarely reviews credit information and only checks reports when applying for financing.

The second spends twenty minutes each month reviewing balances, monitoring utilization, and checking for unusual activity.

Over several years, the second individual is more likely to catch errors quickly, identify potential fraud, maintain healthier utilization levels, and avoid unpleasant surprises.

The difference is not intelligence or income.

It is simply consistent awareness.

This demonstrates why learning to Monitor Your Credit Effectively can create long-term benefits.

Common Credit Monitoring Mistakes

Even consumers who monitor their credit sometimes make mistakes.

Common examples include:

- Checking only the score.

- Ignoring account details.

- Overlooking utilization trends.

- Failing to review reports.

- Waiting until applying for credit.

- Ignoring suspicious activity.

Effective monitoring involves understanding the entire credit picture rather than focusing on a single number.

How Credit Monitoring Supports Better Financial Decisions

Credit monitoring is not simply about avoiding problems.

It can also improve decision-making.

When you understand your credit profile, you can make more informed choices about:

- Applying for new credit.

- Managing utilization.

- Reducing debt.

- Planning major purchases.

- Improving financial goals.

Knowledge creates confidence, and confidence often leads to better financial decisions.

Related Article: Credit Score Improvement Strategies

Related Article: How to Build Credit Responsibly

Frequently Asked Questions

How often should I check my credit?

For most consumers, a monthly review is sufficient to stay informed and identify potential issues.

Does checking my own credit hurt my score?

Generally, reviewing your own credit information does not negatively affect your credit score.

Should I monitor my score or my report?

Both are important. The score provides a summary, while the report explains the factors influencing that score.

What should I do if I find an error?

Review the information carefully and contact the appropriate organization responsible for reporting the account.

Why does my score change even when I pay on time?

Credit scores are influenced by multiple factors, including utilization, account balances, and recently reported information.

Can monitoring improve my credit score?

Monitoring alone does not improve scores, but it helps identify issues and supports better financial decisions that may improve credit over time.

Additional Resources for Credit Monitoring

Financial education remains one of the most effective ways to strengthen long-term credit health.

For additional information about credit monitoring resources, the Consumer Financial Protection Bureau provides educational tools covering credit reports, credit scores, identity protection, and responsible credit management.

Related Article: Best Ways to Maintain a Healthy Credit Profile

Related Article: Best Credit Habits for Better Financial Health

Final Thoughts

Learning how to Monitor Your Credit Effectively is one of the simplest yet most valuable financial habits you can develop. Regular monitoring helps you identify errors, detect fraud, track progress, and maintain awareness of the factors influencing your credit profile.

The goal is not to obsess over every score change. Instead, focus on staying informed and making consistent financial decisions that support long-term credit health.

Small actions performed regularly often produce the strongest results. By dedicating a little time each month to understanding your credit, you can protect your financial future and avoid many of the problems that catch consumers by surprise.