Financial challenges can affect anyone. Job loss, reduced income, unexpected expenses, economic uncertainty, medical emergencies, and rising living costs can create significant financial pressure. Learning Manage Finances During Difficult Times can help individuals maintain stability, reduce stress, and make smarter financial decisions when money becomes tight.

While difficult periods can feel overwhelming, having a clear financial strategy often makes situations more manageable. The goal is not perfection but maintaining control and protecting financial well-being until circumstances improve.

In 2026, economic uncertainty and increasing expenses make financial resilience more important than ever. Fortunately, practical steps can help households navigate challenging periods successfully.

This guide explains how to manage finances during difficult times and protect your financial future.

Why Financial Planning Matters During Difficult Times

Financial planning becomes even more important during periods of uncertainty.

Benefits include:

- Better spending control

- Reduced financial stress

- Improved cash flow management

- Greater financial confidence

- Protection against emergencies

A clear financial plan can help prevent small problems from becoming larger ones.

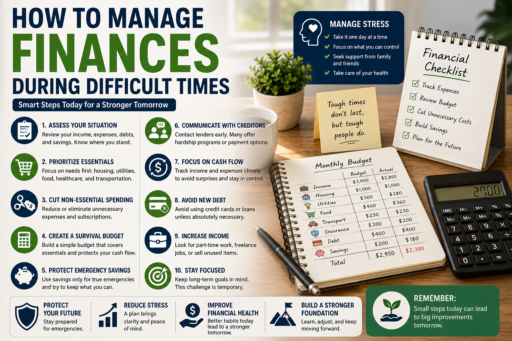

Step 1: Assess Your Financial Situation

The first step in learning Manage Finances During Difficult Times is understanding your current financial position.

Review:

- Income sources

- Savings balances

- Monthly expenses

- Outstanding debts

- Financial obligations

Accurate information allows better decision-making.

Step 2: Prioritize Essential Expenses

When money is limited, essential expenses should receive priority.

Examples include:

- Housing

- Utilities

- Food

- Healthcare

- Transportation

Protecting necessities helps maintain stability during difficult periods.

Step 3: Reduce Non-Essential Spending

Review discretionary expenses and identify areas where temporary reductions may be possible.

Examples include:

- Entertainment subscriptions

- Dining out

- Luxury purchases

- Impulse spending

Small spending reductions can significantly improve cash flow.

One of the most effective ways to Manage Finances During Difficult Times is eliminating unnecessary spending and redirecting available money toward essential expenses and financial stability.

Step 4: Create a Temporary Survival Budget

A survival budget focuses on covering necessities while preserving available resources.

This approach helps:

- Control spending

- Extend savings

- Reduce financial pressure

- Improve cash flow

Temporary adjustments can provide valuable breathing room.

Step 5: Protect Emergency Savings

Emergency funds exist specifically for difficult situations.

Use emergency savings carefully and strategically while continuing to prioritize essential expenses.

Maintaining some financial reserves whenever possible improves resilience.

Step 6: Communicate With Creditors

Many lenders and service providers offer hardship programs during financial difficulties.

Contact providers early if you anticipate problems meeting obligations.

Early communication often creates more options and flexibility.

Step 7: Focus on Cash Flow

Cash flow management becomes critical during challenging times.

Monitor:

- Income timing

- Upcoming bills

- Available savings

- Debt obligations

Understanding cash flow helps avoid financial surprises.

One of the most important ways to Manage Finances During Difficult Times is monitoring cash flow carefully to ensure essential expenses can be covered without unnecessary financial stress.

Step 8: Avoid Unnecessary Debt

While debt may sometimes be unavoidable, unnecessary borrowing can create additional financial pressure.

Carefully evaluate new financial commitments before taking them on.

Limiting debt often improves long-term financial recovery.

Step 9: Look for Additional Income Opportunities

Supplemental income can improve financial flexibility.

Potential options include:

- Freelance work

- Part-time employment

- Selling unused items

- Online opportunities

Additional income may reduce reliance on savings and debt.

Step 10: Stay Focused on Long-Term Goals

Difficult times can make long-term goals seem less important.

However, maintaining awareness of future objectives helps support motivation and financial recovery.

One of the most effective ways to Manage Finances During Difficult Times is maintaining focus on long-term financial goals while adapting to short-term challenges and financial uncertainty.

Common Financial Mistakes During Difficult Times

Even with good intentions, many people make financial mistakes that worsen already difficult situations.

Common mistakes include:

- Ignoring financial problems

- Using high-interest debt excessively

- Failing to create a budget

- Continuing unnecessary spending

- Delaying communication with creditors

Avoiding these mistakes can significantly improve financial stability and recovery prospects.

Manage Financial Stress Effectively

Financial difficulties often create emotional pressure and anxiety.

Learning Manage Finances During Difficult Times also involves managing emotional responses.

Helpful strategies include:

- Focusing on controllable actions

- Creating realistic plans

- Avoiding panic decisions

- Seeking support when needed

Clear thinking often leads to better financial outcomes.

Avoid Emotional Spending

Stress can increase the temptation to make emotional purchases.

Examples include:

- Impulse shopping

- Luxury purchases

- Unplanned online spending

- Retail therapy

Recognizing emotional spending patterns can help protect limited financial resources.

Review Finances Monthly

Regular reviews become even more important during difficult periods.

A monthly review should include:

- Income changes

- Expense reductions

- Savings balances

- Debt obligations

- Recovery progress

Monthly reviews help ensure financial decisions remain aligned with current circumstances.

Adjust Financial Goals Temporarily

Difficult situations may require temporary adjustments to financial goals.

Examples include:

- Reducing savings targets

- Pausing certain investments

- Delaying major purchases

- Prioritizing cash reserves

Flexibility often improves financial resilience without abandoning long-term objectives.

Learning to Manage Finances During Difficult Times requires flexibility, patience, and the ability to adjust financial goals while continuing to work toward long-term financial stability.

Build a Financial Recovery Plan

Recovery becomes easier when supported by a structured plan.

A recovery strategy may include:

- Increasing income

- Reducing expenses

- Paying down debt

- Rebuilding savings

- Tracking progress regularly

Clear recovery plans provide direction and motivation.

Rebuild Emergency Savings

If emergency funds were used during a crisis, rebuilding them should become a priority once financial conditions improve.

Emergency savings help prepare for future challenges and reduce financial vulnerability.

Focus on Long-Term Financial Recovery

The process of Manage Finances During Difficult Times does not end when the immediate crisis passes.

Long-term recovery often involves:

- Strengthening financial habits

- Improving budgeting systems

- Building larger emergency funds

- Diversifying income sources

- Reducing financial risk

These steps can improve financial stability and future preparedness.

Learn From Financial Challenges

Difficult situations often provide valuable lessons.

Questions to consider include:

- What worked well?

- What could be improved?

- Which expenses were unnecessary?

- How can future resilience be strengthened?

Learning from challenges often leads to stronger financial decision-making.

One of the best ways to Manage Finances During Difficult Times is to analyze past financial challenges, identify weaknesses, and apply those lessons to build a more resilient financial future.

Use Trusted Financial Resources

Individuals facing financial difficulties can benefit from trusted educational resources. The Consumer Financial Protection Bureau provides practical guidance on budgeting, debt management, financial recovery, and consumer protection.

Reliable financial information can help individuals make more informed decisions during challenging times.

Additional Resources for Financial Stability

To strengthen your financial foundation, consider reading Save Money on Utility Bills, Break the Paycheck to Paycheck Cycle, and Best Keyword Research Tools for Beginners.

These resources provide practical strategies for improving financial organization, budgeting, and long-term stability.

The Benefits of Financial Resilience

Developing financial resilience can provide:

- Greater confidence

- Improved financial security

- Reduced stress

- Better decision-making

- Stronger long-term stability

Financial resilience helps individuals recover more effectively from future challenges.

Learning to Manage Finances During Difficult Times can strengthen financial resilience and improve long-term financial stability.

Final Thoughts

Learning Manage Finances During Difficult Times is an essential life skill that can help protect financial well-being during periods of uncertainty.

By prioritizing essential expenses, controlling spending, managing cash flow, communicating with creditors, and focusing on long-term recovery, individuals can navigate difficult situations more successfully.

Remember that financial challenges are often temporary. With a clear plan, consistent action, and patience, it is possible to recover, rebuild, and move toward a stronger financial future.