Living paycheck to paycheck is one of the most stressful financial situations many people face. Even individuals with decent incomes sometimes find themselves running out of money before their next paycheck arrives. This cycle can create financial anxiety, limit savings, and make it difficult to achieve long-term goals. Learning Break the Paycheck to Paycheck Cycle can help you build financial stability and gain greater control over your money.

In 2026, rising living costs, subscription services, debt payments, and unexpected expenses make it increasingly difficult for many households to get ahead financially. Fortunately, escaping the paycheck-to-paycheck cycle is possible with the right financial habits and strategies.

The process may not happen overnight, but consistent improvements can create lasting financial change.

This guide explains practical steps to stop living paycheck to paycheck and start building financial security.

Why People Live Paycheck to Paycheck

Many assume paycheck-to-paycheck living only affects low-income earners.

In reality, people at many income levels experience this challenge.

Common causes include:

- High living expenses

- Lack of budgeting

- Excessive debt

- Insufficient savings

- Lifestyle inflation

- Unexpected expenses

Understanding the root causes helps identify solutions.

Signs You’re Living Paycheck to Paycheck

Common warning signs include:

- Running out of money before payday

- Using credit cards for essentials

- Having little or no savings

- Feeling stressed about upcoming bills

- Struggling with unexpected expenses

Recognizing these signs is the first step toward improvement.

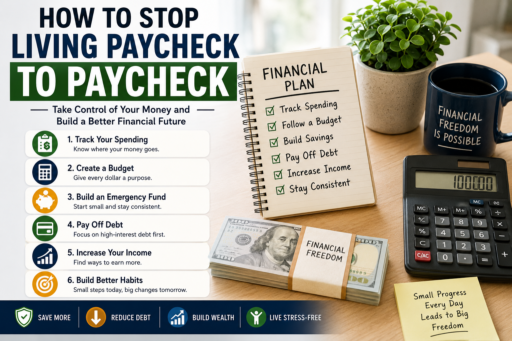

Step 1: Understand Where Your Money Goes

Many people underestimate how much they spend each month.

Before making changes, review your expenses carefully.

Track:

- Housing

- Food

- Transportation

- Subscriptions

- Entertainment

- Debt payments

If you’re looking for practical expense tracking methods, you may also enjoy our guide on Best Ways to Track Your Daily Expenses.

Financial awareness creates opportunities for improvement.

Step 2: Create a Realistic Budget

A budget provides a plan for your money.

Without a budget, spending often becomes reactive rather than intentional.

An effective budget should include:

- Essential expenses

- Savings goals

- Debt payments

- Personal spending

The goal is balance, not extreme restriction.

Step 3: Build a Small Emergency Fund

Unexpected expenses often push people deeper into the paycheck-to-paycheck cycle.

Even a modest emergency fund can help.

Initial goals may include:

- $500

- $1,000

- One month of expenses

Emergency savings provide financial flexibility during difficult situations.

If you’re starting from zero, you may also find our guide on Build an Emergency Fund From Scratch helpful.

Step 4: Reduce Unnecessary Expenses

Small spending reductions can create significant savings over time.

Areas to review include:

- Unused subscriptions

- Food delivery

- Impulse purchases

- Premium memberships

- Convenience spending

The objective is not eliminating enjoyment but reducing waste.

Step 5: Avoid Lifestyle Inflation

Many people increase spending whenever income rises.

This behavior makes it difficult to improve financial security.

Instead of increasing spending immediately, consider directing additional income toward:

- Savings

- Debt reduction

- Investments

This approach accelerates financial progress.

Step 6: Pay Off High-Interest Debt

Debt can consume a significant portion of monthly income.

High-interest balances often make it difficult to build savings.

Prioritizing debt reduction can free up cash flow and reduce financial stress.

Step 7: Automate Good Financial Habits

Automation helps remove decision fatigue.

Consider automating:

- Savings transfers

- Bill payments

- Investment contributions

Automation supports consistency and reduces missed opportunities.

Why Financial Discipline Matters

Escaping the paycheck-to-paycheck cycle often requires behavioral change.

Consistent habits usually produce better results than dramatic short-term efforts.

Financial discipline helps maintain progress over time.

Focus on Progress, Not Perfection

Financial improvement is rarely a straight line.

Unexpected setbacks happen to everyone.

The important thing is continuing to move forward rather than giving up after a difficult month.

Small improvements repeated consistently often create significant long-term results.

Step 8: Increase Your Income

While reducing expenses is important, increasing income can accelerate financial progress significantly.

Additional income opportunities may include:

- Freelancing

- Part-time work

- Online businesses

- Selling digital products

- Career advancement

Even modest increases in income can create extra room for savings and debt reduction.

Step 9: Prioritize High-Interest Debt

Debt often keeps people trapped in the paycheck-to-paycheck cycle.

High-interest balances can consume money that could otherwise be used for savings or investments.

Common debt reduction approaches include:

- Debt Avalanche Method

- Debt Snowball Method

- Balance consolidation

- Extra monthly payments

Reducing debt improves monthly cash flow and financial flexibility.

Family Budgeting Strategies

Families often face additional financial responsibilities, making budgeting even more important.

Helpful family budgeting habits include:

- Creating shared financial goals

- Reviewing expenses together

- Planning major purchases

- Tracking household spending

- Building emergency savings

Working together often improves budgeting success.

If you’re managing household finances, you may also enjoy our guide on Best Budgeting Tools for Families.

Create Financial Breathing Room

Financial breathing room means having money available after paying bills and expenses.

Ways to create more breathing room include:

- Reducing recurring expenses

- Increasing income

- Refinancing expensive debt

- Improving budgeting accuracy

Even small improvements can reduce financial stress significantly.

Common Mistakes That Keep People Stuck

Many people unknowingly remain trapped in the paycheck-to-paycheck cycle because of recurring financial mistakes.

Examples include:

- Ignoring budgets

- Overspending on lifestyle upgrades

- Using credit cards for essentials

- Failing to build savings

- Not tracking expenses

Avoiding these mistakes can accelerate financial improvement.

Build Better Money Habits

Learning Break the Paycheck to Paycheck Cycle strategies often comes down to developing stronger financial habits.

Helpful habits include:

- Tracking expenses weekly

- Saving automatically

- Reviewing budgets monthly

- Planning purchases carefully

- Avoiding emotional spending

Small habits practiced consistently often create powerful long-term results.

Why Emergency Savings Matter

Without emergency savings, unexpected expenses can quickly create financial setbacks.

Emergency funds help cover:

- Medical bills

- Car repairs

- Home maintenance

- Temporary income loss

Financial security improves when unexpected expenses no longer create panic.

Track Financial Progress

Progress tracking helps maintain motivation.

Consider monitoring:

- Savings growth

- Debt reduction

- Monthly spending

- Net worth improvements

Visible progress encourages continued effort.

Focus on Long-Term Financial Stability

The goal is not simply surviving until the next paycheck.

The goal is creating financial stability that allows you to:

- Save consistently

- Handle emergencies

- Reduce stress

- Build wealth

- Achieve financial goals

Long-term stability provides greater freedom and confidence.

Use Trusted Financial Resources

People interested in improving money management skills can benefit from trusted educational resources. The Consumer Financial Protection Bureau provides practical guidance on budgeting, saving, debt management, and financial planning.

Reliable financial education helps strengthen long-term financial habits.

The Benefits of Escaping the Paycheck-to-Paycheck Cycle

Breaking free from paycheck-to-paycheck living can improve nearly every area of personal finance.

Benefits include:

- Reduced financial stress

- Increased savings

- Greater financial confidence

- Improved decision-making

- Better long-term financial security

These improvements often create positive momentum that continues for years.

Final Thoughts

Learning how to Break the Paycheck to Paycheck Cycle requires patience, consistency, and financial awareness.

By understanding where your money goes, creating a realistic budget, reducing unnecessary expenses, building emergency savings, paying down debt, and increasing income where possible, you can gradually improve your financial situation.

Progress may not happen overnight, but every positive financial decision moves you closer to greater stability, security, and long-term financial success.