Managing household finances effectively is essential for achieving financial stability and long-term security. Whether you live alone, share expenses with a spouse, or support a growing family, having a clear financial plan can reduce stress and improve decision-making. Learning the Strategies for Managing Household Finances can help families control spending, increase savings, reduce debt, and work toward important financial goals.

In 2026, households face numerous financial challenges, including rising living costs, subscriptions, insurance expenses, transportation costs, and unexpected emergencies. Without a structured approach, these expenses can quickly become overwhelming.

Fortunately, successful household financial management does not require complicated systems. Consistent habits and practical strategies often produce the best results.

This guide explores proven strategies for managing household finances more effectively.

These Strategies for Managing Household Finances can help families improve budgeting, increase savings, and achieve long-term financial stability.

Why Household Financial Management Matters

Strong household financial management helps:

- Reduce financial stress

- Increase savings

- Control spending

- Improve communication

- Build long-term financial security

When finances are organized, families can focus more on their goals and less on money-related problems.

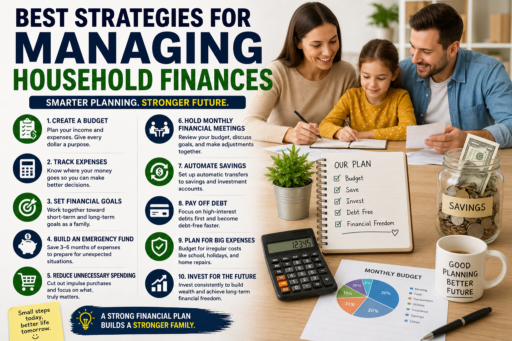

Strategy #1: Create a Household Budget

A budget serves as the foundation of household financial management.

A household budget should include:

- Total income

- Housing expenses

- Utilities

- Food costs

- Transportation

- Savings contributions

- Debt payments

A clear budget helps ensure every dollar has a purpose.

Strategy #2: Track Household Expenses

Many families underestimate their monthly spending.

Tracking expenses helps identify:

- Spending leaks

- Unnecessary purchases

- Budgeting opportunities

- Areas for improvement

Financial awareness is one of the most powerful money management tools.

Strategy #3: Set Shared Financial Goals

Households often achieve better results when everyone works toward common objectives.

Examples include:

- Emergency funds

- Debt reduction

- Home ownership

- Vacation savings

- Retirement planning

Shared goals improve motivation and financial cooperation.

Strategy #4: Build an Emergency Fund

Unexpected expenses can disrupt even the best financial plans.

Emergency savings help cover:

- Medical bills

- Vehicle repairs

- Home maintenance

- Temporary income loss

A financial safety net improves household stability and confidence.

Strategy #5: Reduce Unnecessary Spending

Small spending reductions can create meaningful savings over time.

Common areas to review include:

- Unused subscriptions

- Impulse purchases

- Food delivery services

- Premium memberships

Reducing wasteful spending creates additional room in the budget.

Strategy #6: Hold Monthly Financial Meetings

Regular financial discussions help ensure everyone remains informed and aligned.

Topics may include:

- Budget performance

- Savings progress

- Upcoming expenses

- Financial goals

Open communication often prevents financial misunderstandings.

Strategy #7: Automate Savings

Automation helps make saving consistent.

Consider automatic transfers for:

- Emergency funds

- Retirement savings

- Investment accounts

- Major financial goals

Automation reduces the temptation to spend money intended for savings.

Strategy #8: Prioritize Debt Reduction

Debt can limit financial flexibility and increase stress.

Many households benefit from focusing on:

- Credit card debt

- Personal loans

- High-interest balances

Reducing debt often frees up additional money for savings and investments.

Strategy #9: Prepare for Large Expenses

Major expenses are easier to manage when planned in advance.

Examples include:

- School costs

- Vehicle maintenance

- Home repairs

- Holiday spending

Dedicated savings categories help prevent financial surprises.

Strategy #10: Focus on Long-Term Stability

Successful household finances are built through consistent decisions over time.

Rather than seeking quick fixes, focus on sustainable habits that support long-term financial health and security.

Common Family Budgeting Mistakes

Even households with good intentions sometimes make financial mistakes that slow progress.

Common mistakes include:

- Not following a budget consistently

- Failing to track expenses

- Ignoring savings goals

- Overspending on non-essential items

- Not communicating about money

Identifying and correcting these mistakes can significantly improve household finances.

Managing Finances With Children

Children add both joy and financial responsibility to a household.

Parents can strengthen financial management by:

- Planning education expenses

- Creating dedicated savings funds

- Budgeting for activities and hobbies

- Teaching basic money skills

Financial planning becomes easier when future expenses are anticipated in advance.

Teaching Financial Responsibility at Home

Households can use everyday situations to teach children valuable money lessons.

Examples include:

- Saving for desired purchases

- Comparing prices

- Understanding needs versus wants

- Setting financial goals

These lessons can create lifelong financial habits.

Successful Strategies for Managing Household Finances require regular reviews and consistent financial planning.

Conduct Monthly Household Financial Reviews

A monthly financial review helps ensure household finances remain on track.

Review topics may include:

- Total spending

- Budget performance

- Savings growth

- Debt reduction progress

- Upcoming expenses

Regular reviews make it easier to identify problems and adjust plans when necessary.

Create Dedicated Savings Categories

Many households save more successfully when money is assigned to specific goals.

Examples include:

- Emergency savings

- Home maintenance

- Vacation funds

- Education savings

- Vehicle replacement funds

Dedicated savings categories improve organization and financial discipline.

Plan for Seasonal Expenses

Certain expenses occur every year but are often forgotten.

Examples include:

- School supplies

- Holiday spending

- Insurance renewals

- Vehicle registration

- Home maintenance projects

Planning ahead helps prevent financial surprises.

Use Technology to Simplify Money Management

Budgeting apps and financial tools can help households stay organized.

Technology can assist with:

- Expense tracking

- Budget monitoring

- Savings goals

- Bill reminders

- Financial reporting

Digital tools often improve consistency and financial awareness.

Household Wealth-Building Strategies

The Strategies for Managing Household Finances should not focus solely on reducing expenses.

Long-term financial growth also requires:

- Consistent saving

- Debt reduction

- Emergency funds

- Investment contributions

- Income growth opportunities

Wealth is typically built through small, consistent actions repeated over many years.

Improve Communication About Money

Financial disagreements often occur when expectations are unclear.

Helpful communication practices include:

- Discussing goals openly

- Reviewing budgets together

- Planning major purchases jointly

- Sharing financial responsibilities

Strong communication supports stronger financial outcomes.

Use Trusted Financial Resources

Families interested in improving money management skills can benefit from trusted educational resources. The Consumer Financial Protection Bureau provides practical guidance on budgeting, saving, debt management, and financial planning.

Reliable financial education strengthens long-term financial decision-making.

Additional Financial Resources

To further improve your household finances, consider reading Manage Money More Effectively Every Month, Best Budget Templates for Personal Finance, and Reduce Unnecessary Monthly Expenses.

These resources complement household budgeting strategies and provide practical financial guidance.

The Long-Term Benefits of Effective Household Financial Management

Strong household financial management can provide:

- Greater financial security

- Reduced stress

- Improved savings

- Better financial communication

- Long-term wealth-building opportunities

These benefits often improve both financial stability and overall quality of life.

The most effective Strategies for Managing Household Finances combine budgeting, saving, communication, and long-term planning.

Final Thoughts

The Strategies for Managing Household Finances focus on budgeting, communication, planning, saving, and long-term financial discipline.

By tracking expenses, creating shared goals, reducing unnecessary spending, building emergency savings, and conducting regular financial reviews, households can create a stronger financial foundation.

Remember that financial success is rarely the result of a single decision. Instead, it is built through consistent habits and smart choices that support long-term stability and growth.