Financial goals provide direction, motivation, and a clear purpose for managing money. Without specific goals, it becomes easy to spend impulsively, save inconsistently, and lose focus on long-term financial success. Learning Set Realistic Financial Goals can help you create a practical roadmap that improves financial stability and increases the likelihood of achieving important milestones.

Many people fail to reach their financial goals because they set targets that are too ambitious, too vague, or disconnected from their current financial situation. Realistic goals balance ambition with practicality, making progress measurable and achievable.

In 2026, financial planning is more important than ever due to rising living costs, economic uncertainty, and increasing financial responsibilities. Setting realistic financial goals can help you stay focused regardless of external challenges.

This guide explains how to create realistic financial goals and improve your chances of long-term success.

Why Financial Goals Matter

Financial goals help transform good intentions into concrete actions.

Benefits include:

- Better money management

- Improved motivation

- Increased savings

- Reduced financial stress

- Greater financial confidence

Goals provide a clear reason for budgeting, saving, and making smarter financial decisions.

Understand Your Current Financial Situation

The first step in learning Set Realistic Financial Goals is understanding your starting point.

Review:

- Income

- Expenses

- Savings

- Debt

- Investments

Accurate information helps create goals that are both realistic and achievable.

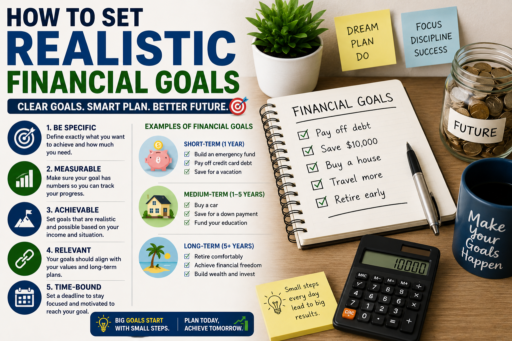

Different Types of Financial Goals

Financial goals generally fall into three categories.

Short-Term Goals

- Building an emergency fund

- Paying off small debts

- Saving for a vacation

Medium-Term Goals

- Purchasing a vehicle

- Saving for education

- Expanding investments

Long-Term Goals

- Retirement planning

- Home ownership

- Financial independence

Using multiple goal categories creates a balanced financial strategy.

Use the SMART Goal Framework

One of the most effective methods for goal setting is the SMART framework.

Goals should be:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

For example, “Save $3,000 for an emergency fund within 12 months” is more effective than simply saying “save more money.”

Prioritize Your Goals

Many people have multiple financial objectives.

Common priorities include:

- Emergency savings

- Debt reduction

- Retirement contributions

- Investment growth

Prioritization helps ensure limited resources are used effectively.

Break Large Goals Into Smaller Milestones

Large financial goals can feel overwhelming.

Breaking goals into smaller milestones makes progress easier to track.

For example:

- Goal: Save $12,000

- Monthly target: $1,000

- Weekly target: Approximately $230

Smaller milestones often increase motivation and consistency.

Create a Dedicated Savings Plan

Every financial goal should have a funding strategy.

Consider:

- Automatic transfers

- Dedicated savings accounts

- Monthly contribution targets

A clear savings plan turns goals into actionable financial habits.

Track Progress Regularly

Monitoring progress helps maintain momentum.

Track:

- Savings growth

- Debt reduction

- Investment contributions

- Goal completion percentages

Visible progress often increases commitment and motivation.

Avoid Unrealistic Expectations

One of the biggest financial planning mistakes is setting goals that are too aggressive.

Unrealistic goals often lead to:

- Frustration

- Loss of motivation

- Abandoned plans

Realistic goals encourage consistent progress and long-term success.

Adjust Goals When Necessary

Life circumstances change.

Income, expenses, family responsibilities, and economic conditions may require adjustments.

Flexibility helps keep goals relevant and achievable.

Common Financial Goal-Setting Mistakes

Even people who are highly motivated can struggle to achieve financial goals if their planning process is flawed.

Common mistakes include:

- Setting unrealistic targets

- Failing to track progress

- Having too many goals at once

- Not creating a savings plan

- Ignoring changing financial circumstances

Avoiding these mistakes can significantly improve your chances of success.

Family Financial Goals

Financial goals become even more important when multiple people share financial responsibilities.

Common family financial goals include:

- Building an emergency fund

- Saving for education

- Purchasing a home

- Reducing household debt

- Planning family vacations

Shared goals often improve accountability and financial cooperation.

Create Goals for Different Life Stages

Financial priorities often change throughout life.

Young professionals may focus on:

- Emergency savings

- Career development

- Debt reduction

Families may focus on:

- Housing

- Education costs

- Retirement planning

Aligning goals with life stages helps maintain relevance and motivation.

Long-Term Wealth-Building Goals

While short-term goals provide quick wins, long-term goals often have the greatest financial impact.

Examples include:

- Retirement savings

- Investment growth

- Financial independence

- Passive income generation

Long-term goals encourage consistent saving and investing habits.

Connect Goals to Daily Financial Decisions

Financial goals should influence everyday spending behavior.

Before making major purchases, ask:

- Does this support my goals?

- Will this delay my progress?

- Is this purchase necessary?

This habit helps align spending with long-term priorities.

Use Visual Progress Tracking

Many people remain motivated when they can see progress.

Helpful tracking methods include:

- Savings charts

- Goal trackers

- Budgeting apps

- Progress spreadsheets

Visible progress often increases consistency and commitment.

Review Financial Goals Monthly

Financial goals should not be set and forgotten.

A monthly review can help:

- Measure progress

- Identify obstacles

- Adjust savings targets

- Refine priorities

Regular reviews keep goals realistic and achievable.

Celebrate Milestones

Achieving financial goals takes time.

Celebrating milestones can help maintain motivation and reinforce positive habits.

Examples include:

- Reaching savings targets

- Paying off debt

- Completing investment goals

Small celebrations can make long-term goals feel more rewarding.

Stay Flexible During Financial Challenges

Unexpected events can temporarily slow progress.

Examples include:

- Medical expenses

- Job changes

- Economic downturns

- Family emergencies

Flexibility allows you to adapt without abandoning your financial plan entirely.

Use Trusted Financial Resources

People interested in improving financial planning skills can benefit from trusted educational resources. The Consumer Financial Protection Bureau offers practical guidance on budgeting, saving, debt management, and financial goal setting.

Reliable financial education can improve both goal setting and long-term financial outcomes.

Additional Resources for Financial Success

To strengthen your financial planning strategy, consider reading Strategies for Managing Household Finances, Manage Money More Effectively Every Month, and Best Money-Saving Challenges.

These resources complement financial goal setting and provide practical money management guidance.

The Long-Term Benefits of Financial Goals

Setting realistic financial goals can provide:

- Greater financial clarity

- Improved saving habits

- Reduced financial stress

- Better decision-making

- Long-term financial security

Consistent progress toward meaningful goals often leads to greater financial confidence and success.

Final Thoughts

Learning Set Realistic Financial Goals is one of the most important skills for long-term financial success.

By understanding your current financial situation, creating achievable targets, tracking progress regularly, and adjusting plans when necessary, you can build a financial roadmap that supports both short-term needs and long-term dreams.

Remember that financial success is rarely achieved through a single decision. Instead, it comes from setting clear goals and taking consistent action over time.