Most people think improving credit is all about paying bills on time. While payment history is certainly important, strong credit is often the result of dozens of financial decisions made consistently over many months and years.

Imagine two people with similar incomes. One regularly reviews finances, plans spending carefully, manages debt responsibly, and thinks long-term. The other makes financial decisions impulsively, ignores account balances, and rarely monitors credit activity.

Several years later, their credit profiles may look dramatically different.

The difference is rarely luck. More often, it is the result of everyday choices.

Learning the Best Financial Decisions That Improve Credit can help you strengthen your credit profile, reduce borrowing costs, increase financial flexibility, and create better opportunities in the future.

The good news is that many of the most effective decisions are simple. They do not require a high income, advanced financial knowledge, or complicated strategies. Instead, they require consistency and awareness.

In this guide, we’ll explore some of the most valuable financial decisions consumers can make to improve and maintain healthy credit over time.

Why Financial Decisions Matter More Than Quick Fixes

Many consumers search for shortcuts when trying to improve credit.

They look for quick score increases, rapid credit-building tactics, or instant solutions.

Unfortunately, strong credit rarely develops that way.

Credit profiles generally reflect long-term behavior. Lenders are often more interested in patterns than isolated actions.

This is why smart financial decisions tend to produce better results than temporary credit hacks.

Small positive actions repeated consistently can have a powerful cumulative effect.

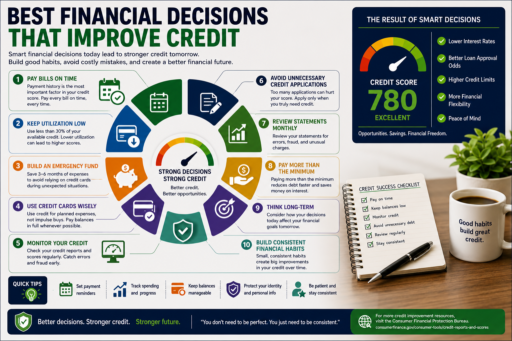

Decision #1: Always Pay Bills on Time

If there is one decision that consistently supports stronger credit health, it is making on-time payments a priority.

Many consumers underestimate how much influence payment history can have over the long term.

Imagine paying every bill on time for several years.

That consistent behavior demonstrates reliability and financial responsibility.

To improve consistency:

- Use automatic payments when appropriate.

- Set reminders before due dates.

- Review accounts regularly.

- Create a monthly bill-payment routine.

Simple systems often prevent costly mistakes.

Decision #2: Keep Credit Utilization Low

One of the smartest financial decisions consumers can make is managing utilization carefully.

Many people focus entirely on making payments while overlooking how much available credit they are using.

Imagine carrying balances that regularly approach your credit limits.

Even if payments are made on time, high utilization can create unnecessary pressure on your credit profile.

Keeping balances manageable often supports healthier long-term outcomes.

Related Article: How Credit Utilization Affects Your Score

Decision #3: Build an Emergency Fund

At first glance, emergency savings may not seem connected to credit improvement.

In reality, emergency funds often protect credit during difficult situations.

Unexpected expenses are a normal part of life.

Vehicle repairs, medical costs, home maintenance, and temporary income disruptions can occur at any time.

Without savings, many consumers rely heavily on credit cards.

An emergency fund provides flexibility and reduces dependence on borrowed money when challenges arise.

Decision #4: Use Credit Cards Strategically

Credit cards can either strengthen financial health or create long-term problems depending on how they are used.

Responsible consumers typically view credit cards as financial tools rather than additional income.

Healthy habits often include:

- Paying balances on time.

- Avoiding unnecessary purchases.

- Monitoring spending.

- Keeping balances manageable.

These habits can help support long-term credit improvement while reducing financial stress.

Related Article: How to Build Credit Responsibly

Decision #5: Monitor Credit Regularly

One of the most overlooked financial decisions is making credit monitoring a routine habit.

Many people only review their credit when applying for financing.

Unfortunately, waiting until you need a loan may allow problems to go unnoticed.

Regular monitoring can help identify:

- Reporting errors.

- Fraud indicators.

- Utilization changes.

- Credit improvement opportunities.

Awareness is often the first step toward improvement.

Decision #6: Avoid Applying for Credit Unnecessarily

Modern consumers are constantly exposed to credit offers.

Rewards cards, promotional financing, special offers, and pre-approved applications can make borrowing seem harmless.

However, one of the smartest Financial Decisions That Improve Credit is learning to be selective.

Before applying for any new account, ask yourself:

- Do I genuinely need this credit product?

- Will it improve my financial situation?

- Can I manage it responsibly?

- Am I applying because of a need or a promotion?

Intentional borrowing usually produces better long-term outcomes than impulsive borrowing.

Decision #7: Review Financial Statements Every Month

Many consumers only glance at statements long enough to make a payment.

Unfortunately, this habit can allow problems to go unnoticed.

Monthly reviews often help identify:

- Unexpected charges.

- Growing balances.

- Spending trends.

- Subscription increases.

- Potential fraud.

Think of statement reviews as financial maintenance.

A few minutes each month can prevent larger problems later.

Decision #8: Pay More Than the Minimum When Possible

Minimum payments can help consumers remain current on accounts, but relying on them indefinitely often slows financial progress.

Imagine carrying a balance for several years while paying only the minimum amount required.

Interest charges continue accumulating, and debt reduction becomes much slower.

Paying even a little extra each month may reduce interest costs and help balances decline faster.

Small improvements repeated consistently can create meaningful long-term results.

Decision #9: Think Long-Term Before Making Financial Choices

Many financial mistakes happen because decisions are made with today’s emotions rather than tomorrow’s goals in mind.

Before making an important borrowing decision, consider the long-term impact.

Could this purchase create financial pressure next month?

How will this decision affect your future goals?

Will the benefit still feel worthwhile a year from now?

People with strong credit profiles often develop the habit of evaluating decisions through a long-term lens.

Decision #10: Build Consistent Financial Habits

One of the most valuable lessons in personal finance is that success rarely comes from a single decision.

Instead, it is usually the result of consistent habits.

Examples include:

- Paying bills on time.

- Tracking expenses.

- Monitoring credit.

- Maintaining savings.

- Managing debt responsibly.

These habits may seem simple individually, but together they create a strong foundation for long-term credit health.

Related Article: Best Credit Habits for Better Financial Health

A Real-Life Example of Better Financial Decisions

Consider two individuals who start with similar incomes and similar credit scores.

The first person creates a budget, builds emergency savings, reviews accounts monthly, and uses credit carefully.

The second person spends impulsively, ignores account balances, and rarely monitors financial activity.

Five years later, the difference in their financial situations may be significant.

The first individual often enjoys lower debt, stronger credit, and greater financial flexibility.

The second may face higher balances, increased stress, and fewer borrowing opportunities.

The difference is not necessarily income or intelligence.

It is the result of better financial decisions repeated consistently over time.

How Better Decisions Create Better Credit

Credit improvement is often viewed as a separate goal.

In reality, stronger credit is usually a byproduct of stronger financial habits.

Consumers who make better decisions regarding spending, saving, borrowing, and planning often improve their credit naturally over time.

This is why focusing exclusively on credit scores can sometimes be less effective than improving overall financial behavior.

Related Article: Best Ways to Maintain a Healthy Credit Profile

Related Article: How to Avoid Common Credit Mistakes

Frequently Asked Questions

What financial decision improves credit the most?

Consistently paying bills on time remains one of the most important decisions supporting long-term credit health.

Can emergency savings improve credit?

Indirectly, yes. Emergency savings may reduce reliance on credit cards and help consumers manage unexpected expenses responsibly.

How often should I monitor my credit?

Many consumers benefit from reviewing their credit information monthly to identify changes and monitor progress.

Should I avoid credit cards completely?

Not necessarily. When used responsibly, credit cards can help establish positive payment history and support credit-building efforts.

Can better financial habits improve credit scores?

Yes. Healthy habits often contribute to stronger credit profiles over time because credit scores reflect financial behavior.

How long does it take to see credit improvement?

The timeline varies, but consistent positive decisions often produce gradual improvements over months and years.

Additional Resources for Credit Improvement

Financial education can help consumers make smarter decisions and maintain stronger credit profiles.

For additional information about credit improvement resources, the Consumer Financial Protection Bureau provides educational tools covering credit reports, credit scores, and responsible credit management.

Related Article: Credit Score Improvement Strategies

Related Article: Best Starter Credit Cards for Young Adults

Final Thoughts

The best Financial Decisions That Improve Credit are often simple, practical, and completely within your control. Paying bills on time, managing utilization wisely, maintaining emergency savings, monitoring credit activity, and making thoughtful borrowing decisions can all contribute to stronger long-term credit health.

Credit improvement rarely happens overnight. Instead, it develops through consistent actions that demonstrate responsibility and financial discipline.

The encouraging news is that every positive decision moves you in the right direction. Over time, those decisions can lead to stronger credit, greater financial flexibility, lower borrowing costs, and increased confidence in your financial future.