Imagine spending years working hard to improve your financial situation. One important part of building a strong financial profile is to avoid common credit mistakes. You pay your bills, earn a steady income, and try to make responsible decisions. Then one day, you apply for a loan or credit card and discover that your credit profile is not as strong as you expected.

For many people, this situation is not caused by a lack of income or financial knowledge. Instead, it is often the result of small credit mistakes that gradually accumulate over time.

Some mistakes happen because of misunderstanding. Others occur because of poor habits, lack of attention, or simple financial stress. The frustrating part is that many of these errors are completely avoidable.

Learning how to Avoid Common Credit Mistakes can help protect your credit score, reduce financial stress, improve borrowing opportunities, and strengthen your long-term financial health.

The good news is that you do not need perfect finances to maintain healthy credit. In most cases, avoiding a handful of common mistakes can make a significant difference over time.

In this guide, we’ll examine the most frequent credit mistakes consumers make and discuss practical strategies for avoiding them.

Why Small Credit Mistakes Matter

Many people expect credit problems to result from major financial disasters.

In reality, credit damage often begins with small behaviors repeated consistently.

Imagine forgetting a payment once.

Or allowing balances to remain high for several months.

Or applying for several credit products within a short period.

Individually, these actions may not seem serious.

Over time, however, they can gradually weaken a credit profile and create unnecessary financial obstacles.

This is why awareness matters so much. Recognizing mistakes early is often easier than repairing damage later.

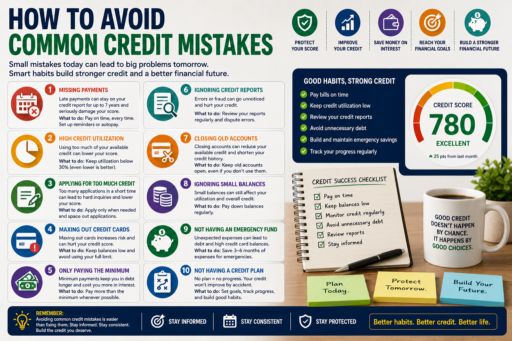

Mistake #1: Missing Payment Deadlines

If there is one mistake that consistently appears in weakened credit profiles, it is late payments.

Many consumers do not miss payments because they lack money. Instead, they forget due dates, overlook statements, or lose track of financial obligations.

Imagine paying every bill on time for years and then missing several payments simply because life became busy.

The impact can be frustrating because it is entirely preventable.

Simple solutions include:

- Automatic payments.

- Calendar reminders.

- Mobile banking alerts.

- Monthly financial reviews.

Creating systems reduces reliance on memory and helps prevent costly mistakes.

Mistake #2: Ignoring Credit Utilization

Many consumers focus entirely on payments while ignoring how much credit they are using.

This is where utilization becomes important.

Imagine two individuals with identical payment histories.

One consistently uses a small portion of available credit.

The other regularly carries balances close to credit limits.

Even though both pay on time, lenders may view these situations differently.

Monitoring utilization helps maintain a healthier credit profile and may support stronger credit outcomes over time.

Related Article: How Credit Utilization Affects Your Score

Mistake #3: Applying for Too Much Credit Too Quickly

New credit accounts can sometimes be beneficial.

However, applying for multiple products within a short period may create unnecessary risk.

Imagine receiving promotional offers for several credit cards.

Opening all of them immediately may seem harmless, but it can complicate financial management and increase borrowing temptation.

Consumers who successfully Avoid Common Credit Mistakes typically apply for credit with a clear purpose rather than reacting to every available offer.

Mistake #4: Treating Credit Cards Like Extra Income

This mistake is responsible for countless financial problems.

Credit cards provide access to borrowed money—not additional income.

Imagine receiving a salary increase of $500 per month.

That increase belongs to you.

A $5,000 credit limit does not.

Consumers who blur this distinction often accumulate debt faster than they realize.

The healthiest approach is viewing credit cards as financial tools rather than spending opportunities.

Related Article: How to Build Credit Responsibly

Mistake #5: Focusing Only on Credit Scores

Many people become obsessed with a single number.

While credit scores are important, they do not tell the entire story.

A strong credit profile involves:

- Payment history.

- Utilization management.

- Account history.

- Financial discipline.

- Responsible borrowing habits.

People who focus exclusively on scores sometimes overlook the behaviors that actually influence those scores.

Mistake #6: Never Reviewing Credit Reports

Many consumers assume that if they pay bills on time, there is no reason to review their credit reports.

Unfortunately, that assumption can be costly.

Credit reports may occasionally contain reporting errors, outdated information, or activity that deserves further investigation.

Imagine discovering an error only after applying for a mortgage or auto loan. Correcting the problem at that stage can be stressful and time-consuming.

Regular reviews help consumers identify issues early and maintain greater control over their financial profiles.

Related Article: How to Monitor Your Credit Effectively

Mistake #7: Making Only Minimum Payments Forever

Minimum payments can be useful during temporary financial challenges.

The problem occurs when minimum payments become a long-term strategy.

Imagine carrying a balance for years while only paying the minimum amount due each month.

A large portion of those payments may go toward interest rather than reducing the actual balance.

This often slows financial progress and increases the overall cost of borrowing.

Whenever possible, consumers should aim to pay more than the minimum and gradually reduce outstanding balances.

Mistake #8: Closing Old Accounts Without a Plan

Many people believe closing unused credit cards automatically improves credit health.

In reality, the decision is often more complicated.

Older accounts may contribute to the overall age of your credit history and provide additional available credit that helps support lower utilization percentages.

This does not mean every old account should remain open forever. However, closing accounts without understanding the potential consequences can sometimes create unexpected results.

Before closing an account, consider how it fits within your overall financial strategy.

Mistake #9: Ignoring Financial Problems Until They Become Serious

One of the most damaging habits in personal finance is avoidance.

Many consumers notice warning signs but postpone action.

Perhaps balances are increasing.

Maybe expenses are exceeding income.

Or perhaps debt feels slightly more difficult to manage each month.

Small financial issues rarely improve on their own.

The earlier problems are addressed, the easier they usually become to solve.

Consumers who Avoid Common Credit Mistakes tend to face challenges directly rather than hoping they disappear.

Mistake #10: Failing to Build Emergency Savings

At first glance, emergency savings may seem unrelated to credit.

In reality, they are closely connected.

Imagine your vehicle suddenly requires a major repair or an unexpected medical expense appears.

Without emergency savings, many people immediately rely on credit cards.

This can increase utilization, create additional debt, and place pressure on future budgets.

Even a modest emergency fund can help protect credit health during unexpected situations.

A Real-Life Example of How Small Mistakes Add Up

Consider two individuals with similar incomes and similar financial goals.

The first person monitors accounts regularly, pays bills on time, maintains emergency savings, and keeps utilization under control.

The second occasionally misses due dates, ignores statements, carries high balances, and rarely reviews financial information.

Neither person experiences a major financial disaster.

However, after several years, their credit profiles may look dramatically different.

The difference is not luck.

It is the result of hundreds of small decisions repeated over time.

This example highlights why avoiding mistakes is often just as important as adopting positive financial habits.

How Good Habits Prevent Most Credit Problems

The encouraging news is that most credit mistakes are preventable.

Simple habits often provide significant protection.

Examples include:

- Reviewing accounts monthly.

- Paying bills on time.

- Monitoring utilization.

- Tracking financial goals.

- Maintaining emergency savings.

- Using credit responsibly.

These habits may seem ordinary, but their long-term impact can be substantial.

Related Article: Best Ways to Maintain a Healthy Credit Profile

Frequently Asked Questions

What is the most common credit mistake?

Late payments remain one of the most common and potentially damaging credit mistakes because payment history plays an important role in overall credit health.

Can high credit utilization hurt my score even if I pay on time?

Yes. High utilization may affect your credit profile even when payments are made consistently.

How often should I review my credit report?

Many consumers benefit from reviewing credit reports several times per year to identify errors and monitor progress.

Should I close unused credit cards?

Not always. Consider the impact on account age and available credit before making a decision.

Can emergency savings help protect my credit?

Yes. Emergency savings may reduce reliance on credit cards during unexpected financial situations.

How long does it take to recover from credit mistakes?

Recovery depends on the specific situation, but consistent positive habits often help strengthen credit profiles over time.

Additional Resources for Credit Education

Financial education remains one of the most effective ways to avoid mistakes and improve long-term credit health.

For additional information about credit education resources, the Consumer Financial Protection Bureau provides educational tools covering credit reports, credit scores, and responsible credit management.

Related Article: Credit Score Improvement Strategies

Related Article: How to Read a Credit Card Statement

Final Thoughts

Learning how to Avoid Common Credit Mistakes is one of the simplest ways to protect your financial future. Most credit problems do not appear overnight. Instead, they develop gradually through habits, oversights, and decisions that seem minor in the moment.

The good news is that many of these mistakes are entirely preventable. Paying bills on time, monitoring utilization, reviewing reports, maintaining emergency savings, and using credit responsibly can help you build a stronger financial foundation.

Remember that successful credit management is rarely about perfection. It is about consistency. Small positive actions repeated month after month often create the strongest long-term results and the healthiest credit profiles.