Many beginners receive their first credit card statement and immediately feel overwhelmed by the numbers, payment details, balances, and unfamiliar financial terms. However, learning how to read a credit card statement is one of the most important financial skills for managing credit responsibly.

Your statement contains valuable information about your spending habits, payment obligations, interest charges, rewards, and account activity. Understanding these details can help you avoid debt, protect your credit score, and improve your financial decisions.

Fortunately, credit card statements become much easier to understand once you know what each section means.

In this beginner-friendly guide, you will learn:

- What a credit card statement is

- How to understand each section

- What balances and payments mean

- How interest is shown

- How to spot fees and mistakes

- How statements affect your credit score

- Common beginner mistakes to avoid

What Is a Credit Card Statement in How to Read a Credit Card Statement?

A credit card statement is a monthly summary of your credit card activity provided by your card issuer.

It usually includes:

- Your purchases

- Payments made

- Current balance

- Minimum payment due

- Interest charges

- Fees

- Rewards activity

- Payment due date

Statements are important because they help you track spending, avoid missed payments, and identify financial problems early.

Why How to Read a Credit Card Statement Matters

Understanding your statement can help you:

- Avoid late payments

- Reduce interest charges

- Catch fraud quickly

- Monitor subscriptions

- Track spending habits

- Protect your credit score

According to Consumer Financial Protection Bureau, regularly reviewing statements helps consumers better manage debt and detect billing errors.

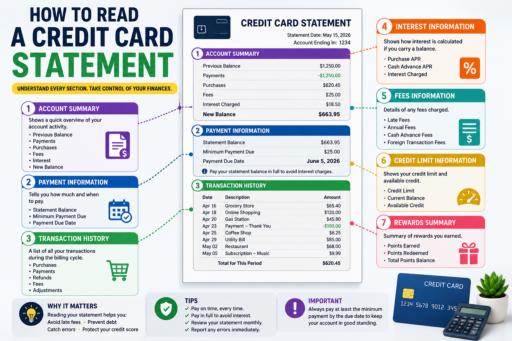

Account Summary Section

The account summary is usually displayed near the top of the statement.

This section gives a quick overview of your account.

Common Information Included

- Previous balance

- Payments received

- New purchases

- Fees charged

- Interest added

- Current balance

This section helps you quickly understand how your balance changed during the billing cycle.

Current Balance Explained

Your current balance is the total amount you currently owe.

This includes:

- Purchases

- Interest charges

- Fees

- Unpaid balances

However, your current balance may continue changing after the statement date if you make additional purchases.

Statement Balance vs Current Balance

Many beginners confuse these two balances.

Statement Balance

The amount owed when the billing cycle closed.

Current Balance

The live balance including recent activity after the statement closed.

Paying the statement balance in full usually helps you avoid interest charges.

Minimum Payment Due

The minimum payment is the smallest amount required to keep your account in good standing.

While paying the minimum prevents late fees temporarily, it may still allow interest to accumulate.

Therefore, paying the full statement balance is usually the better strategy.

Learn more in our guide on How to Avoid Credit Card Interest.

Payment Due Date

Your due date is the deadline for making payments.

Missing this date may cause:

- Late fees

- Higher APR rates

- Credit score damage

- Interest charges

Many people use automatic payments to avoid missing due dates.

Transaction History Section

This section lists all activity during the billing cycle.

Typical Transactions Include

- Store purchases

- Online shopping

- Subscriptions

- Refunds

- Payments

- Cash advances

Reviewing transaction history carefully helps detect:

- Fraudulent charges

- Billing mistakes

- Forgotten subscriptions

- Overspending habits

Interest Charges Section

This section explains how much interest you were charged during the billing cycle.

It may include:

- Purchase APR

- Cash advance APR

- Penalty APR

- Total interest charged

If you consistently pay balances in full, this section may show zero interest.

APR Explained

APR stands for Annual Percentage Rate.

It represents the yearly cost of borrowing money using your card.

Common APR types include:

- Purchase APR

- Balance transfer APR

- Cash advance APR

- Penalty APR

Higher APR rates make carrying balances more expensive.

Fees Section

Your statement may also display fees charged during the billing cycle.

Common Fees Include

- Late payment fees

- Annual fees

- Foreign transaction fees

- Cash advance fees

- Balance transfer fees

Monitoring fees regularly helps avoid unnecessary costs.

Credit Limit Information

Your statement also displays your total available credit limit.

Example:

- Credit limit = $5,000

- Current balance = $1,000

- Available credit = $4,000

This information is important because it affects your credit utilization ratio.

Understanding Credit Utilization

Credit utilization measures how much of your available credit you are using.

Experts generally recommend staying below 30% utilization.

High utilization may hurt your credit score.

For a deeper explanation, read our article on Best Cash Back Strategies to Maximize Rewards.

Rewards Section

If your card offers rewards, your statement may display:

- Cash back earned

- Reward points

- Travel miles

- Bonus categories

Reviewing rewards regularly helps ensure you receive the benefits your card offers.

How Statements Affect Your Credit Score

Your statement balance may be reported to credit bureaus.

This can affect:

- Credit utilization

- Payment history

- Credit score changes

Paying balances before the statement closing date may help lower reported utilization.

How to Spot Fraud or Billing Errors

Carefully reviewing statements helps identify unauthorized transactions quickly.

Watch for:

- Unknown purchases

- Duplicate charges

- Incorrect amounts

- Suspicious subscriptions

If you notice suspicious activity, contact your card issuer immediately.

How to Read a Credit Card Statement More Easily

Beginners can simplify statements by focusing on these key sections first:

- Current balance

- Statement balance

- Due date

- Minimum payment

- Interest charges

- Recent transactions

Once you understand these sections, the rest becomes much easier.

Best Beginner Habits for Managing Statements

- Review statements monthly

- Pay balances in full

- Track subscriptions

- Monitor interest charges

- Use automatic payments

- Watch utilization levels

These habits help prevent long-term financial problems.

Common Beginner Mistakes

1. Ignoring Statements

Some people never review statements carefully.

2. Paying Only Minimum Payments

This often increases long-term interest costs.

3. Missing Due Dates

Late payments can damage your credit score.

4. Not Monitoring Subscriptions

Small recurring charges can grow over time.

5. Ignoring Interest Charges

Interest can accumulate surprisingly fast.

How to Use Statements to Improve Financial Habits

Your statement can become a powerful budgeting tool.

By reviewing spending patterns monthly, you can:

- Reduce unnecessary purchases

- Identify spending triggers

- Improve budgeting

- Pay down debt faster

If you want better organization, read our article on Secured Credit Cards vs Unsecured Cards.

Final Thoughts on How to Read a Credit Card Statement

Learning how to read a credit card statement may seem difficult at first, but it becomes much easier with practice. Understanding your balances, due dates, interest charges, and transactions can help you avoid debt, protect your credit score, and improve your financial habits.

The key is consistency.

Reviewing statements regularly helps you stay informed, organized, and financially responsible.

Most importantly, remember that your statement is not just a bill — it is a valuable financial tool that can help you make smarter money decisions long-term.