Choosing the right credit card is an important step when building credit for the first time. However, many beginners become confused when comparing secured credit cards vs unsecured cards because both types work differently and serve different financial purposes.

Understanding the difference between these cards can help you choose the best option for your financial situation, credit history, and long-term goals.

For people with no credit history or poor credit, secured credit cards may provide a safer starting point. Meanwhile, unsecured cards are more common for people with stronger credit profiles and established financial histories.

In this beginner-friendly guide, you will learn:

- What secured credit cards are

- What unsecured credit cards are

- The biggest differences between both card types

- Which option is better for beginners

- How secured cards help build credit

- Common mistakes to avoid

- How to choose the right card in 2026

What Are Secured Credit Cards in Secured Credit Cards vs Unsecured Cards?

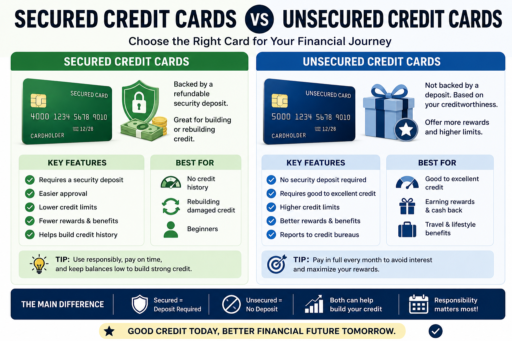

A secured credit card is a credit card backed by a refundable security deposit.

This deposit reduces the lender’s risk because it acts as collateral if payments are not made.

For example:

- You deposit $300

- Your credit limit becomes approximately $300

Secured cards are commonly designed for:

- Beginners with no credit history

- People rebuilding damaged credit

- Individuals recovering from financial problems

Even though secured cards require deposits, they still function similarly to regular credit cards.

What Are Unsecured Credit Cards?

An unsecured credit card does not require a security deposit.

Instead, approval depends mainly on:

- Credit score

- Income

- Debt levels

- Payment history

Most traditional credit cards are unsecured cards.

These cards usually offer:

- Higher credit limits

- Better rewards

- Lower fees

- Travel benefits

- Cash back programs

However, unsecured cards may be harder to obtain for beginners with limited credit history.

Why Secured Credit Cards vs Unsecured Cards Matters

Choosing the correct type of card can affect:

- Your approval chances

- Your ability to build credit

- Your financial flexibility

- Your long-term borrowing opportunities

Understanding the differences helps beginners avoid applying for cards they may not qualify for.

According to Experian, secured cards can help people establish or rebuild credit when used responsibly.

Main Difference Between Secured and Unsecured Cards

| Feature | Secured Cards | Unsecured Cards |

|---|---|---|

| Security Deposit | Required | Not Required |

| Approval Difficulty | Easier | Harder |

| Rewards | Limited | Usually Better |

| Credit Limit | Often Lower | Often Higher |

| Best For | Building/Rebuilding Credit | Established Credit Users |

How Secured Credit Cards Help Build Credit

Secured cards can help build credit because most issuers report payment activity to major credit bureaus.

Responsible usage includes:

- Paying on time

- Keeping balances low

- Avoiding overspending

- Using cards consistently

Over time, these habits may improve your credit score significantly.

If you want to understand credit scores better, read our guide on How to Improve Your Credit Score Faster.

Do Secured Cards Hurt Your Credit?

No — secured cards themselves do not hurt your credit.

In fact, they can improve your score if managed responsibly.

Problems only occur if you:

- Miss payments

- Max out the card

- Carry high balances

Responsible behavior matters far more than the type of card itself.

Benefits of Secured Credit Cards

1. Easier Approval

Because of the security deposit, lenders accept more applicants with limited or poor credit.

2. Helps Build Credit History

Regular on-time payments may strengthen your credit profile.

3. Lower Risk for Beginners

Smaller limits may reduce overspending temptation.

4. Possible Upgrade Opportunities

Some secured cards eventually upgrade to unsecured cards after responsible usage.

Disadvantages of Secured Credit Cards

1. Requires Upfront Deposit

The biggest downside is needing cash upfront.

2. Lower Credit Limits

Most secured cards start with smaller limits.

3. Fewer Rewards

Many secured cards offer limited benefits compared to unsecured cards.

4. Possible Fees

Some secured cards charge annual or maintenance fees.

Benefits of Unsecured Credit Cards

1. No Security Deposit

You do not need to provide upfront collateral.

2. Better Rewards Programs

Many unsecured cards offer:

- Cash back

- Travel rewards

- Bonus categories

- Purchase protections

3. Higher Credit Limits

Established users often receive larger spending limits.

4. More Premium Features

Some cards include:

- Airport lounge access

- Travel insurance

- Extended warranties

Disadvantages of Unsecured Credit Cards

1. Harder Approval Requirements

Applicants usually need stronger credit profiles.

2. Higher Risk of Overspending

Larger limits may tempt some users into unnecessary debt.

3. Interest Can Become Expensive

Carrying balances may lead to costly interest charges.

Learn more in our article on How to Avoid Credit Card Interest.

Which Card Is Better for Beginners?

The answer depends on your current financial situation.

Choose a Secured Card If:

- You have no credit history

- You were denied traditional cards

- You are rebuilding credit

- You want a safer starting point

Choose an Unsecured Card If:

- You already have decent credit

- You qualify for beginner unsecured cards

- You want rewards and better features

Can Secured Cards Become Unsecured Cards?

Yes.

Some issuers review accounts after several months of responsible usage.

If approved, they may:

- Refund your deposit

- Convert the account into an unsecured card

- Increase your credit limit

This transition can be a major milestone for beginners building credit.

How Credit Utilization Affects Both Card Types

Both secured and unsecured cards are affected by credit utilization.

Credit utilization measures how much of your available credit you use.

Experts usually recommend keeping balances below 30%.

For a deeper explanation, read our article on Credit Utilization Explained for Beginners.

Common Beginner Mistakes

1. Maxing Out the Card

Using all available credit may hurt your score.

2. Missing Payments

Late payments can damage credit quickly.

3. Applying for Too Many Cards

Too many applications may lower approval chances temporarily.

4. Ignoring Fees

Always review annual fees and hidden charges carefully.

5. Closing Cards Too Early

Older accounts may help strengthen credit history.

How to Use Any Credit Card Responsibly

Whether secured or unsecured, responsible habits matter most.

Good habits include:

- Paying on time

- Keeping balances low

- Tracking spending carefully

- Using a monthly budget

- Avoiding unnecessary debt

If you want better financial habits, read our article on How to Use Credit Cards Responsibly.

Best Beginner Strategy for 2026

If you are starting from zero credit, a secured card is often the safest option.

Focus on:

- Making small purchases

- Paying balances fully

- Keeping utilization low

- Building consistent payment history

After improving your credit profile, you may qualify for stronger unsecured cards with better rewards and benefits.

Final Thoughts on Secured Credit Cards vs Unsecured Cards

Understanding secured credit cards vs unsecured cards is essential for beginners trying to build strong financial habits and improve their credit profiles.

Secured cards provide a safer starting point for people with limited or damaged credit, while unsecured cards offer more rewards and flexibility for qualified users.

The most important factor is not the type of card itself — it is how responsibly you use it.

Focus on:

- Paying on time

- Keeping balances low

- Avoiding unnecessary debt

- Tracking spending carefully

With consistent habits and patience, either type of card can help you build a healthier financial future.