As income increases, many people naturally increase their spending. While earning more money can improve financial security and quality of life, it can also create a hidden financial problem known as lifestyle inflation. Learning Prevent Lifestyle Inflation can help you build wealth, increase savings, and achieve long-term financial goals instead of simply spending more as your income grows.

Lifestyle inflation occurs when spending rises alongside income. A salary increase, promotion, bonus, or successful business venture may lead to larger purchases, more expensive habits, and higher monthly expenses. Over time, these changes can prevent meaningful financial progress despite earning significantly more money.

In 2026, social media influence, online shopping, subscription services, and consumer culture make lifestyle inflation more common than ever. Fortunately, there are practical strategies that can help maintain financial discipline while still enjoying income growth.

This guide explains Prevent Lifestyle Inflation and use income increases to strengthen your financial future.

What Is Lifestyle Inflation?

Lifestyle inflation refers to increasing spending whenever income rises.

Examples include:

- Moving to a more expensive home

- Buying a luxury vehicle

- Dining out more frequently

- Purchasing premium subscriptions

- Increasing discretionary spending

While occasional upgrades may be reasonable, uncontrolled lifestyle inflation can limit wealth-building opportunities.

Why Lifestyle Inflation Can Be Dangerous

Many people assume financial success comes from earning more money.

However, financial progress often depends on what you keep rather than what you earn.

Learning Prevent Lifestyle Inflation helps preserve income growth and turn it into long-term financial security.

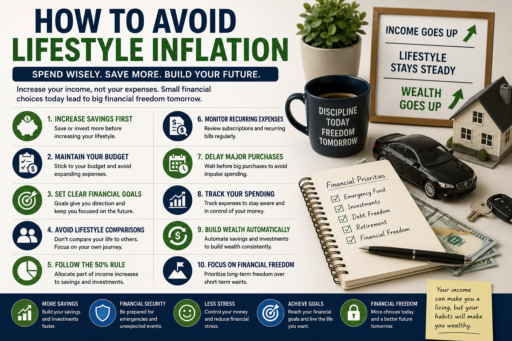

Strategy #1: Increase Savings Before Spending

Whenever income increases, consider increasing savings contributions before adjusting spending habits.

This may include:

- Emergency funds

- Retirement savings

- Investment accounts

- Debt repayment

Prioritizing savings helps ensure income growth improves financial health.

Strategy #2: Maintain Your Existing Budget

Many people immediately expand spending after receiving raises.

Instead, continue following your current budget whenever possible.

Maintaining spending levels allows additional income to strengthen your financial position.

Strategy #3: Define Financial Goals Clearly

Clear goals help resist unnecessary spending.

Examples include:

- Buying a home

- Building wealth

- Retirement planning

- Achieving financial independence

Goals provide motivation to save rather than spend every additional dollar.

People who Prevent Lifestyle Inflation often find it easier to stay committed to long-term financial goals and avoid unnecessary spending increases.

Strategy #4: Avoid Lifestyle Comparisons

Social comparison often fuels lifestyle inflation.

People frequently feel pressure to match the spending habits of friends, coworkers, or influencers.

Focusing on personal goals instead of comparisons can reduce unnecessary spending.

Strategy #5: Follow the 50% Rule

Some financial experts recommend allocating only part of any income increase toward lifestyle improvements.

For example:

- 50% toward savings and investing

- 50% toward lifestyle improvements

This approach allows enjoyment of income growth while maintaining financial progress.

Strategy #6: Monitor Recurring Expenses

Recurring expenses often increase gradually and unnoticed.

Review:

- Subscriptions

- Memberships

- Insurance policies

- Service plans

Regular reviews help prevent unnecessary spending growth.

Regular reviews of recurring expenses can help Prevent Lifestyle Inflation by identifying costs that gradually increase over time.

Strategy #7: Delay Major Purchases

Income increases can create temptation to make immediate purchases.

Consider waiting before making significant financial commitments.

Delays often improve decision-making and reduce impulse spending.

Strategy #8: Track Spending Carefully

Expense tracking increases awareness and accountability.

Understanding where money goes helps identify signs of lifestyle inflation early.

Financial awareness is one of the most effective tools for controlling spending.

Strategy #9: Build Wealth Automatically

Automation can reduce the temptation to spend additional income.

Consider automatic transfers to:

- Savings accounts

- Investment accounts

- Retirement plans

Automation supports long-term financial growth.

Automatic savings and investment contributions are powerful tools to Prevent Lifestyle Inflation because extra income is redirected toward wealth-building before it can be spent.

Strategy #10: Focus on Financial Freedom

The ultimate goal is not simply earning more money but achieving greater financial security and flexibility.

Keeping this perspective can make it easier to avoid unnecessary lifestyle inflation.

Common Lifestyle Inflation Mistakes

Many people unintentionally increase spending as income grows.

Common mistakes include:

- Upgrading homes too quickly

- Buying expensive vehicles after promotions

- Increasing subscription services unnecessarily

- Using raises to support impulse spending

- Ignoring long-term financial goals

Learning Prevent Lifestyle Inflation starts with recognizing these behaviors before they become permanent habits.

Create a Plan for Every Raise

One of the most effective ways to control lifestyle inflation is creating a plan before additional income arrives.

Consider allocating future raises toward:

- Savings goals

- Debt repayment

- Investments

- Emergency funds

People who understand Prevent Lifestyle Inflation often make financial decisions before receiving additional income.

Review Spending Habits Monthly

Monthly financial reviews can help identify spending increases before they become problematic.

Review:

- Monthly expenses

- Subscription costs

- Dining expenses

- Shopping habits

- Discretionary spending

Regular reviews create awareness and improve financial discipline.

The best way to Prevent Lifestyle Inflation is to monitor spending consistently and make adjustments whenever expenses begin rising faster than income.

Focus on Value Instead of Status

Many purchases associated with lifestyle inflation are driven by status rather than genuine value.

Before upgrading your lifestyle, ask:

- Will this improve my life meaningfully?

- Does this align with my goals?

- Can I comfortably afford it?

- Is there a better alternative?

These questions often prevent unnecessary spending decisions.

Build Long-Term Wealth Habits

Wealth is typically built through consistent financial habits rather than occasional large decisions.

Examples include:

- Saving regularly

- Investing consistently

- Living below your means

- Tracking expenses

- Reviewing goals monthly

Individuals who practice Avoid Lifestyle Inflation often develop stronger long-term wealth-building habits.

Use Automation to Protect Income Growth

Automatic transfers can help prevent additional income from being absorbed into higher spending.

Automation may include:

- Investment contributions

- Savings transfers

- Retirement contributions

- Debt payments

Automating financial priorities often improves consistency.

Maintain Financial Flexibility

Higher spending commitments can reduce financial flexibility.

By controlling lifestyle inflation, individuals often maintain:

- Greater savings capacity

- Lower financial stress

- More investment opportunities

- Better emergency preparedness

Flexibility can be one of the greatest financial advantages.

Monitor Long-Term Financial Progress

Instead of focusing only on income growth, measure:

- Net worth growth

- Savings rates

- Debt reduction

- Investment balances

These metrics provide a clearer picture of financial success.

Use Trusted Financial Resources

Individuals interested in improving financial habits can benefit from trusted educational resources. The Consumer Financial Protection Bureau provides practical guidance on budgeting, saving, debt management, and financial planning.

Financial education can help individuals make more informed decisions as income increases.

Additional Resources for Smarter Money Management

To strengthen your financial future, consider reading Financial Checklists for Every Month, Simple Financial Habits That Improve Your Wealth, and Break the Paycheck to Paycheck Cycle.

These resources provide practical strategies for controlling spending, improving financial discipline, and building long-term wealth.

The Benefits of Avoiding Lifestyle Inflation

People who learn Prevent Lifestyle Inflation often experience:

- Higher savings rates

- Greater financial security

- Reduced financial stress

- Faster wealth accumulation

- Improved financial freedom

Small spending decisions repeated consistently can create significant financial advantages over time.

Final Thoughts

Learning Prevent Lifestyle Inflation is one of the most valuable financial skills for long-term wealth building.

By controlling spending, prioritizing savings, automating financial goals, and focusing on value instead of status, you can ensure that income growth improves your financial future rather than simply increasing expenses.

Remember that financial success is not determined by how much money you earn alone. It is determined by how effectively you manage and grow the money you keep.