Many people regularly check their credit score but rarely take the time to review their credit report. Unfortunately, this means they may miss valuable information that could affect their financial future.

Your credit score is only a number. Your credit report tells the story behind that number.

Imagine applying for a mortgage, auto loan, or new credit card and discovering information on your report that you never noticed before. An inaccurate balance, an unfamiliar account, or an old reporting error could potentially affect important financial decisions.

This is why learning how to Understand Credit Reports is such an important financial skill.

A credit report contains detailed information about your borrowing history, payment behavior, account activity, and overall credit profile. Understanding how to read this information can help you identify problems, monitor progress, and make better financial decisions.

The good news is that credit reports are not nearly as complicated as they first appear.

Once you understand the major sections and what information to look for, reviewing your report becomes much easier.

In this guide, we’ll break down the key components of a credit report and explain how to use that information to strengthen your financial health.

Why Credit Reports Matter

Many consumers focus exclusively on their credit scores.

While scores are important, lenders often review information contained within credit reports when evaluating applications.

Your report provides a detailed record of how you have managed credit over time.

It may include:

- Personal information.

- Credit accounts.

- Payment history.

- Credit inquiries.

- Public records when applicable.

Understanding this information can help consumers recognize strengths, identify weaknesses, and maintain greater control over their financial profiles.

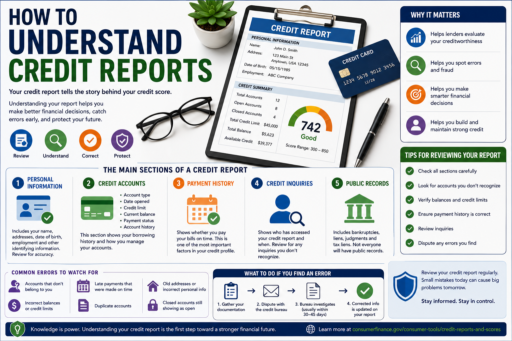

The Main Sections of a Credit Report

Although report formats may vary, most reports contain several common sections.

Learning how these sections work makes it much easier to Understand Credit Reports effectively.

Personal Information

This section typically contains identifying information associated with your credit profile.

Examples may include:

- Name.

- Current and previous addresses.

- Date of birth.

- Employment information when reported.

While this section does not directly affect your score, accuracy remains important.

Incorrect personal information could create confusion or indicate reporting issues that deserve attention.

Credit Accounts

This is often the largest and most important section of the report.

It contains details regarding credit accounts currently open or previously used.

Information may include:

- Account type.

- Date opened.

- Credit limit.

- Current balance.

- Payment status.

- Account history.

This section provides valuable insight into your borrowing behavior and overall credit management habits.

Payment History

One of the most important sections of any credit report involves payment history.

Lenders often want to know whether consumers consistently meet financial obligations.

A strong payment history can demonstrate reliability and responsible credit management.

Conversely, missed payments may signal increased lending risk.

This is one reason why on-time payments remain such an important financial habit.

Understanding Credit Inquiries

Another section many consumers overlook involves credit inquiries.

Inquiries generally occur when credit information is reviewed in connection with financial applications.

For example:

- Credit card applications.

- Auto loans.

- Mortgages.

- Certain financing requests.

Reviewing inquiries can help ensure all activity appears legitimate and expected.

Unexpected inquiries may deserve closer attention.

How Credit Reports Help Detect Problems Early

One of the biggest advantages of reviewing reports regularly is early problem detection.

Imagine discovering an unfamiliar account shortly after it appears rather than several years later.

Or identifying inaccurate account information before applying for important financing.

Consumers who regularly Understand Credit Reports often identify issues faster and respond more effectively.

Related Article: How to Monitor Your Credit Effectively

How to Identify Errors on a Credit Report

One of the most valuable reasons to review a credit report is identifying inaccuracies.

Many consumers assume every detail on a report is automatically correct. While most information is reported accurately, mistakes can occur.

Examples may include:

- Incorrect account balances.

- Accounts that do not belong to you.

- Incorrect payment information.

- Duplicate accounts.

- Outdated personal information.

Even small inaccuracies deserve attention because they may affect your overall credit profile and financial opportunities.

When reviewing reports, take time to compare account information with your own records.

Understanding Negative Information

Many consumers become nervous when they see negative information on a credit report.

However, understanding what appears and why it appears can reduce confusion.

Negative information may include:

- Late payments.

- Accounts in collections.

- Charge-offs.

- Defaults.

- Certain public records when applicable.

The presence of negative information does not necessarily mean your financial future is damaged.

Many consumers successfully improve their credit profiles through consistent positive financial habits over time.

The first step is understanding what information appears on the report and how it may influence lenders’ decisions.

How to Review Account Information Effectively

Simply glancing at a report is rarely enough.

Effective reviews involve examining account details carefully.

When reviewing accounts, consider:

- Are balances accurate?

- Are payment records correct?

- Are account statuses current?

- Do all accounts belong to you?

- Are closed accounts reported properly?

Small discrepancies may be easier to resolve when identified early.

This is one reason consumers who Understand Credit Reports often maintain greater awareness of their financial health.

Why Credit Reports Matter More Than Credit Scores Alone

Many people become fixated on a single score.

While scores provide useful summaries, they do not explain everything.

Imagine two individuals with similar scores.

One may have a long history of responsible borrowing and low utilization.

The other may have recent negative information offset by other positive factors.

The score alone does not tell the entire story.

The credit report provides context that helps explain how a credit profile developed over time.

Understanding both reports and scores creates a more complete financial picture.

How Often Should You Review Your Credit Report?

Many consumers only review reports when applying for financing.

Unfortunately, this approach may allow problems to remain unnoticed for long periods.

Regular reviews can help:

- Identify reporting errors.

- Detect potential fraud.

- Track financial progress.

- Monitor account activity.

- Improve financial awareness.

Think of credit report reviews as routine financial maintenance.

A small amount of attention today can prevent larger problems tomorrow.

Related Article: Best Ways to Maintain a Healthy Credit Profile

A Real-Life Example of Why Reports Matter

Consider a consumer preparing to apply for a mortgage.

Several months before submitting an application, they decide to review their credit report.

During the review, they discover an account showing inaccurate information.

Because the issue is identified early, there is time to investigate and address it before the mortgage process begins.

Now imagine the same issue remaining undiscovered until after the application is submitted.

The situation becomes significantly more stressful.

This example highlights why understanding and reviewing credit reports can provide important financial advantages.

Common Credit Report Mistakes Consumers Make

Many people unintentionally overlook important information.

Common mistakes include:

- Checking only credit scores.

- Ignoring account details.

- Never reviewing reports.

- Failing to monitor inquiries.

- Assuming all information is accurate.

- Waiting until financing is needed.

Consumers who avoid these mistakes often maintain greater control over their credit profiles.

Related Article: Credit Score Improvement Strategies

How Understanding Credit Reports Supports Better Financial Decisions

Knowledge creates confidence.

When consumers understand their reports, they are often better prepared to:

- Apply for credit responsibly.

- Manage utilization effectively.

- Monitor financial progress.

- Identify potential issues.

- Protect long-term financial health.

Rather than reacting to surprises, informed consumers can make proactive decisions that support their financial goals.

Related Article: How to Build Credit Responsibly

Frequently Asked Questions

What is the difference between a credit report and a credit score?

A credit score is a numerical summary of credit information, while a credit report contains the detailed information used to evaluate credit activity and financial behavior.

How often should I review my credit report?

Many consumers benefit from reviewing reports several times per year to monitor accuracy and identify potential issues.

Can errors appear on credit reports?

Yes. While many reports are accurate, errors can occasionally occur and should be reviewed carefully.

Do credit reports show payment history?

Yes. Payment history is often one of the most important sections because it helps demonstrate how financial obligations have been managed over time.

Why are credit inquiries listed?

Inquiries help document situations where credit information has been reviewed in connection with financial applications or account activity.

Additional Resources for Credit Report Education

Understanding how credit reports work can help consumers make better financial decisions and avoid unnecessary surprises.

For additional information about credit report resources, the Consumer Financial Protection Bureau provides educational tools covering credit reports, credit scores, consumer rights, and responsible credit management.

Related Article: Annual Fee vs No Annual Fee Credit Cards

Related Article: Best Financial Decisions That Improve Credit

Final Thoughts

Learning how to Understand Credit Reports is one of the most valuable financial skills consumers can develop. A credit report provides far more information than a simple score and offers important insights into your financial history and credit management habits.

Regular reviews can help identify errors, detect potential fraud, monitor progress, and support smarter financial decisions. Most importantly, understanding your report allows you to take a more active role in protecting your financial future.

The more familiar you become with your credit report, the easier it becomes to maintain strong financial habits and build long-term financial confidence.